Loan rates for small businesses now seven times what they were during pandemic

Average SME loan rate tops 7% as banks’ margins on SME lending return to pre-covid levels alongside higher base rates

Businesses should stress test downside scenarios before they borrow in current interest rate environment

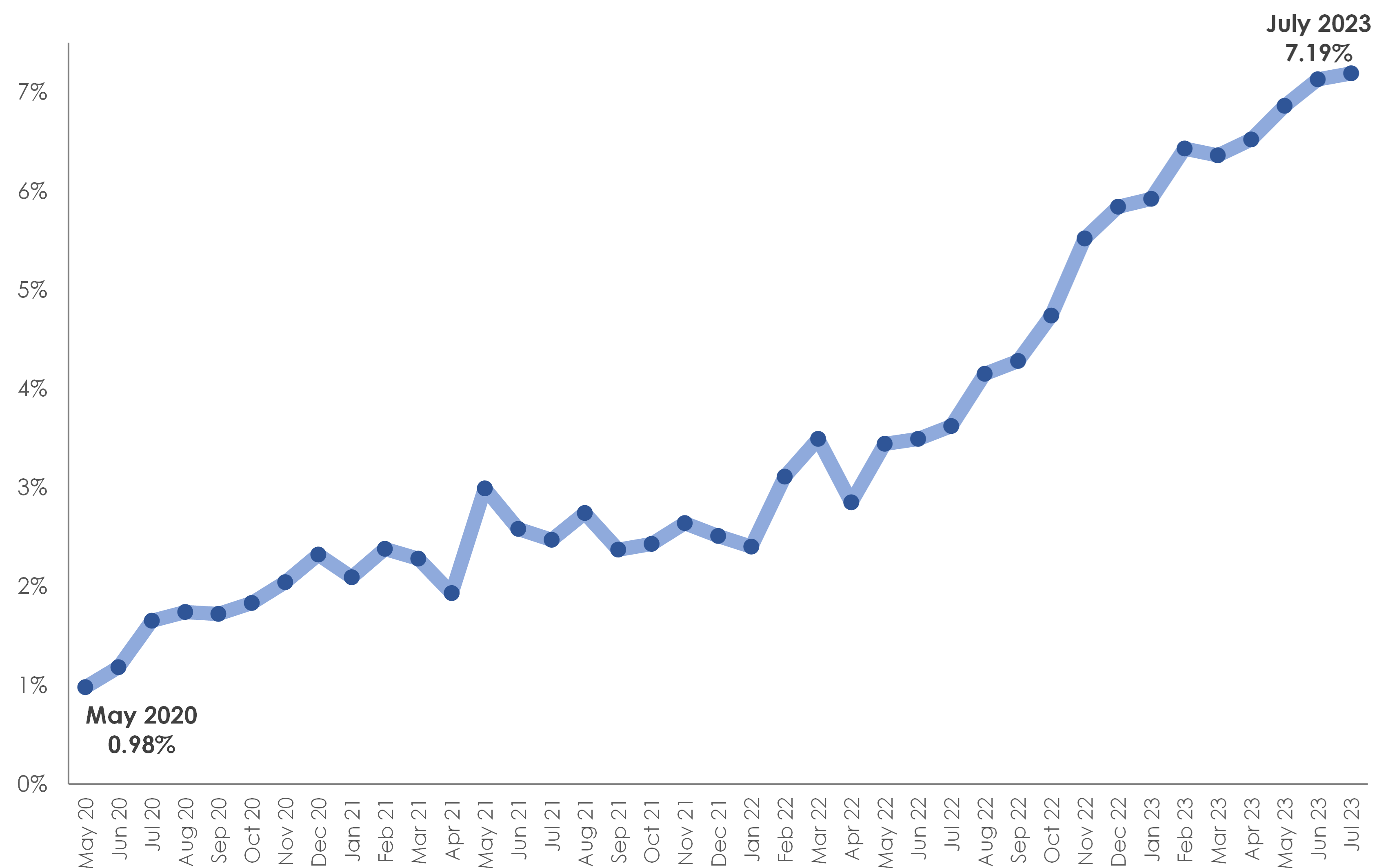

The average interest rate on new loans to small businesses has jumped more than sevenfold from a low of 0.98% in May 2020 to 7.19% in July 2023, says ACP Altenburg Advisory, the debt advisory specialists.

Daniel Barrett, Partner at Altenburg, says that the sharp rise in lending rates for SMEs raises concerns that many small businesses may not be able to afford the debt they need to finance growth opportunities.

The primary driver of the higher interest rates are the increases in the Bank of England’s base rate to try to bring inflation under control.

However, Altenburg’s research also shows that banks’ margins on lending to small businesses have returned to pre-covid levels. In the midst of the pandemic in May 2020, the average interest rate on lending to SMEs stood at 88 basis points above the bank of England’s base rate. In July 2023, the average SME loan rate had increased to 219 basis points above the base rate.

Says Daniel Barrett: “The increase in the margin that lenders are charging SMEs is also due to the higher perceived risk of lending to SMEs in the current unsettled economic conditions. This has exacerbated the impact of the increase in the base rate over the last three years and it is now starting to have a significant impact on SMEs.”

“One of the consequences of a lack of affordable lending will be that some small businesses may choose not to or be unable to borrow to take advantage of growth opportunities. SMEs putting plans for expansion on hold has an adverse impact on economic growth and job creation.”

Daniel Barrett adds that the speed of interest rate rises for SMEs highlights just how important it is for small businesses to choose the most appropriate financing option for their business.

While inflation fell more than expected in August, there are still expectations from some in the market that rates could increase one further time later in the year. Fixed rates offered by lenders take into account market expectations for future base rate movements. This means that it may be possible to secure a fixed rate loan (e.g., by hedging the floating rate using a swap) at a lower rate than the current floating rate interest rate.

Alongside hedging the interest rate, there are other tools (such as price caps) that businesses can use to provide a level of protection against interest rate rises.

Adds Daniel Barrett: “Businesses looking to raise funding should consider taking advice and/or stress testing various downside scenarios before they borrow in the current interest rate environment.”

“There is considerable uncertainty over the path for future interest rate movements, with market expectations proving to be very sensitive to economic news releases, so it’s important for businesses to make sure that they are fully informed on their funding options and the potential impact that they could have on their business and their ability to fund their growth aspirations.”

Average SME lending rate rises SEVENFOLD in just over three years

About ACP Altenburg Advisory

ACP Altenburg Advisory is part of ACP, a leading independent debt advisory association for SME and mid-market companies, advising clients on the options available to them and providing hands on support from day one all the way through to drawdown of the funding raised.

To learn more, please get in touch.

Press contacts

Dan Barrett